Reporting by Michael H. Morris

This quarter’s reports will reflect that the investment markets have generally recovered from the steep losses of the First Quarter. Despite the near round trip in values and all the associated disruption, distraction and drama, the benefit of maintaining a disciplined approach has once again been validated as client portfolios are universally tracking in a manner consistent with their asset allocation and expectations. And yet, with volatility expected to ramp up through the election and year-end, we have re-emphasized resilience as a key characteristic in our evaluations of individual investment opportunities and portfolios. We believe resilient companies are those with fortress competitive positions, low levels of debt, consistent cash flows, growing dividends and the likelihood of surviving/thriving regardless of the external economic environment. We have learned from the pandemic, and in addition to the all-weather resilient companies, we believe there will be clearly defined winners (the maker of our webcams) and those who will face much steeper recovery slopes (anything related to the travel industry). More will surface as opportunities and threats arise around changing business practices and societal views.

There’s more to come later on perceived winners, but can you feel the changes? The media has become fervent in its exertion of pressure attempting to influence public opinion on social injustices, discrimination, climate change and assorted other examples of human imperfection. This message will not opine further on these deeply personal issues; however, we will point out an increasingly prominent and strikingly similar wave of sentiment cresting in the investment world. Investors who formerly may have focused solely on financial returns of investments are loudly extolling the value of non-financial benefits and targeting specific social or environmental outcomes through their commitments of capital. This advent of the “green economy” has resulted in the formalization and intense marketing of an investment approach that considers Environmental, Social and Governance factors in security analysis, security selection, and portfolio management.

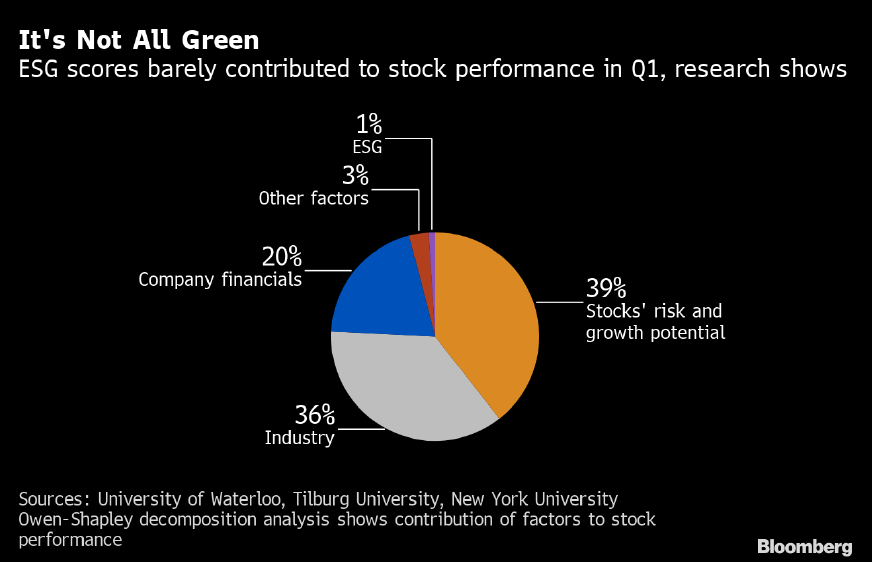

The debate is unsettled as to whether ESG investing is more than just a “Do-good” mentality. Afterall, we are talking about investments, not donations, and at least for most, there still is an expectation of performance. A 2017 study conducted by the Boston Consulting Group offers empirical evidence of better long-term risk-adjusted returns, lower downside and improved volatility in ESG strategies. Economic intuition supports this premise if you consider that companies that ignore ESG factors may miss capturing information and trends that go beyond traditional financial statements in indicating the possibility of higher risk. Proponents of ESG investing have gone as far as suggesting that the application of ESG factors will lead to the holy grail of lower risk AND higher returns. However, research conducted after the first quarter 2020 equity market selloff by New York University’s Stern School of Business suggest that U.S. equities with higher scores on ESG metrics didn’t actually sustain smaller losses, were negatively associated with returns during the second quarter recovery, and more traditional factors like leverage, liquidity and branding had much bigger roles to play in realized returns. All recent research and rhetoric aside, ESG investing factors have not been in place and methodically tracked for a long enough period to accurately assess if values of ESG favored investments are increasing as a result of their underlying style tilt, or if it is simply a function of a massive amount of dollars chasing a limited number of qualifying opportunities.

– Larry Fink, CEO Blackrock

Regardless of whether a company’s values will ultimately and consistently drive the economic value of the company, the momentum surrounding capital flows being directed into ESG investing is difficult to ignore. We are paying attention, but fundamental financial analysis and reasonable valuations are still at the core of how we select companies for investing. To us, profitability is a straightforward barometer. The ability for a company to genuinely make a difference toward the betterment of society is less so. Or at least it seems to be much more subjective with the definition of betterment varying so widely among disparate groups.

We occasionally get accused of seeing the world and the companies in which we invest with rose colored glasses. That optimism, we believe, is important to a consistently successful long-term investment approach. Nevertheless, whether your goal is to manage risk, express your values, callously ride the ESG momentum wave, or pursue righteous performance, it likely will be wise to view the investment opportunities of the future with at least one green lens.