Michael H. Morris, CEO

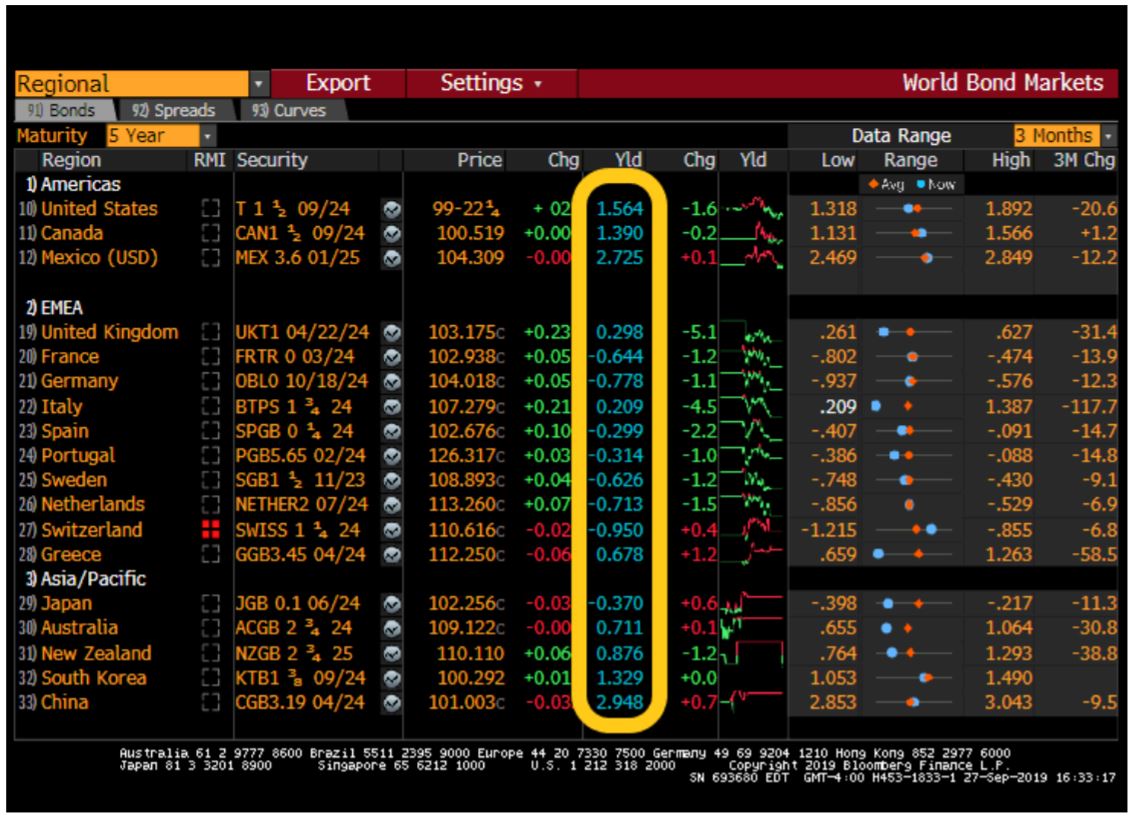

Wait! What? Negative interest rates? You mean interest rates are now so low that depositors must actually pay their banks for the privilege of holding cash? That sounds absurd. While not yet a reality in the U.S., negative interest rate policies have already been adopted by several foreign central banks (European Central Bank, Bank of Japan, and the central banks of Denmark, Sweden and Switzerland), and there is an estimated $16 trillion of negative yielding bonds out of a global bond market that totals roughly $113 trillion, according to the Institute of International Finance. Germany recently issued 30-year zero coupon bonds with a guaranteed return to investors of -0.11%! Meanwhile, in an effort to lock in historically low rates, the U.S. Treasury Department is considering issuing 50 year bonds beginning in 2020. Locking in guaranteed negative returns and/or bond maturity commitments equivalent to more than half a lifetime are not investments most of our clients would want us to make, regardless of the rationale. A snapshot of the world bond market at month-end September reflects the global phenomena, with more major economy countries offering 5-year sovereign debt with negative yields than those with positive returns.

There’s no need for U.S. investors to panic as the Federal Reserve has yet to resort to negative interest rates. In fact, even after the September Fed Funds reduction to a range of 1.75-2.00%, the U.S. remains a global outlier. It’s no surprise that foreign investors are clamoring for U.S. denominated debt, placing further downward pressure on yields. It is becoming increasingly apparent lower for longer yields on fixed-income investments may just be an investment fact of life. That, in turn, requires adjustments, not just to bond return expectations, but also ultimately to portfolio asset allocation. Expect to hear more about this from us.

What? Wait! The media has been all abuzz as short-term interest rates have persistently stayed higher than longer-term rates. And, as noted in our second quarter client letter, such inverted yield curve occurrences have typically been solid harbingers of imminent recession. That may, in fact, be the case, but more and more economists are suggesting an inverted yield curve may not be the reliable recession indicator it once was. We don’t aim to be the ones jumping on the “this time it’s different” bandwagon, but yields, yield curves, and government bond markets have clearly been distorted by unprecedented central bank actions, such as negative interest rates. In years past, issuers of long-term bonds had to offer higher yields in order to attract investors and to compensate them for the possibility of inflation. These days, it seems the biggest worry on every central banker’s mind is not the potential for inflation, but the concern over deflation – price levels falling and people and businesses holding on to cash (instead of spending or investing) with the belief prices will be even lower in the future.

Besides the U.S. and un-investable basket cases like Greece and Italy, Australia is one of the few developed economies with positive yielding sovereign debt, and it is possible our former sister colony may be giving us an advance look at what we have ahead of us. The Reserve Bank of Australia cut interest rates in both June and July, and while the impact has yet to be fully gauged, their position on the front line of the trade war between the U.S. and China certainly appears to be showing evidence of collateral economic uncertainty, if not direct damage. With that as a backdrop, our next investment research trip will take Chief Investment Officer/Trade War Correspondent, John Suddeth “Down Under” to get a firsthand look. John’s Australian update should be in your hands in November.

While John is away visiting current portfolio holdings and potential equity investment opportunities in Australia, the rest of the team will be putting the finishing touches on an internal conversion to a new portfolio management and reporting system. We’ve been training on and exploring the new system over the past couple of months, and we’re very excited about the upgrade to the Tamarac system. We expect you to see enhancements in both the quality and detail of the reports we provide. Beginning with our year-end reports, to be shared around the first few weeks of the new year, you will notice changes in the form of graphs, charts and ordering of information. Additionally, the system will grant our portfolio managers access to enhanced analytical data by which to more effectively manage client assets. It’s new, cool technology, but we continue to understand that the “steak” is more important than the “sizzle”.

We pride ourselves on the meaningfulness of the firm’s continuing commitment to research travel. Not only do we occasionally surface investment opportunities that fly under the radar, but we gain a global perspective that simultaneously broadens the mind and gives us a perspective different than those limited in thought by where they sit or what they read or hear. And, apparently, that insatiable curiosity influences not only all current NGA team members, but former members as well. Founding teammate and longtime client service stalwart, Tracey Maddox, officially retired from the firm in May and promptly left town for an extended across the country travel adventure with her husband, Jeff. Tracey has safely returned from her criss-cross of the country and settled in the relatively quiet Chiefland, Florida with memories, photos and yes, a new perspective. We are grateful for Tracey’s dedication to the firm and our clients, and we hope you will join us in wishing her well in retirement.

This month we begin our 10th year, and it is with nostalgia and gratitude we reflect on our business past and business future. Despite operating daily in a world that occasionally feels chaotic, countered by ever changing client dynamics, we look ahead with enthusiasm, optimism and confidence. Enthusiasm for the team of professionals assembled and committed to serve you. Optimism in capitalism and the long-term ability for mankind to overcome obstacles in the name of betterment. And confidence in our investment approach. Thank you for joining us on the journey!