Reporting by Isaac Codrey, CFA

That’s a lot of negativity, yet we find ourselves feeling quite sanguine. Not because we know this macroeconomic hurricane will avoid landfall. No, it’s because we know that we built the house to withstand hurricane force winds. So, we wanted to take this opportunity to provide a general refresher of what you own and why you own it, which will hopefully result in some measure of comfort through these and future economic storms.

In simplistic terms, if you own a bond, you have lent money to a government or corporate entity and in return, they are paying you interest. At the end of the term, they return the money you lent them. Therefore, bonds have a dual purpose of income and relative stability of principal.

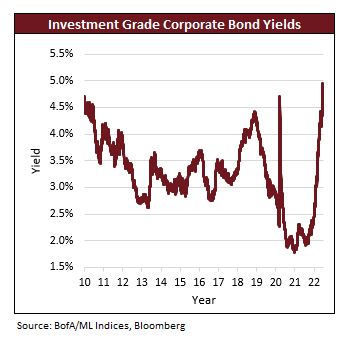

The Fed is projected to raise its benchmark rate to 3.5% by year end which would be the highest level since pre-financial crisis in early 2008. Investors are trying to anticipate these future rate hikes and have already priced them into the bond market. As a result, from a yield perspective, this is one of the more attractive times to be investing in corporate and municipal bonds in the last decade, as highlighted by the corporate bond yield chart below. In contrast to having to accept the miniscule yields offered over the past few years, we are now genuinely excited to be adding bonds to our client portfolios.

In simplistic terms, if you own a stock, you have invested money into a company in return for an ownership stake of its future cash flows (earnings). The stocks that we own have a dual objective of capital appreciation and income.

In particular, NGA’s equity investment philosophy calls for the companies in which we invest to have growing cash flows, for the price of the stock to trade at a discount to our perceived value of the company, and for the company to share its cash flows with its shareholders in the form of a dividend. The first two criteria drive capital appreciation, and the final criteria is the income part of the equation.

Growth: The companies in which we invest have generally experienced rising demand for their products and/or services over the last decade, highlighted by a history of sales and earnings growth. On average, NGA portfolio companies have reported 12% annual earnings expansion over the last five years (which includes a recessionary period). More importantly, we expect them to continue to experience improving demand. Analysts are currently projecting 8% average annual earnings growth the next three years. Admittedly, analysts are rarely 100% correct in their estimates, but a lot of bad stuff (our technical term) has to happen before the revenues of these closely vetted companies flatline, let alone decline. There is a resiliency in NGA portfolio companies’ expansion stories due to their in-demand products/services, healthy margins, and strong balance sheets. As a result, we have great confidence the companies in which we invest will be able to weather the inevitable economic storms, just as they did in 2020 and 2008/09. While values go up and down over the short-term, we are optimistic about NGA portfolio companies continuing to expand their cash flows, which is the ultimate driver of longer-term stock price appreciation.

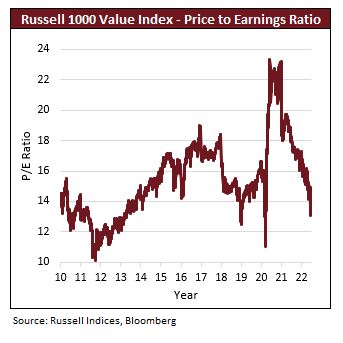

Valuation: Valuations ebb and flow with investor sentiment, and frequently the pendulum swings too far. As recently as three months ago, the market could have been characterized as over-exuberant, filled with speculative investments (e.g., crypto, meme stocks, SPACs), but that has all come crashing down as earnings reality and Fed action work to take the proverbial punch away from the party. As a result, valuations are now swinging to the opposite side of the pendulum. The median Price to Earnings (P/E) multiple on companies in which we invest is around 14.5x. Historically speaking, that represents a very attractive valuation which we have only witnessed in a few periods of distress in the last decade. (The chart below depicts the P/E multiple on the value stocks in the Russell 1000 Index, a good proxy for NGA portfolio companies.) We are quite optimistic about the odds of future success (i.e., capital appreciation) for our clients when we purchase high quality companies at these valuations. Paraphrasing Warren Buffet, “we want to be fearful when others are greedy, and greedy when others are fearful.” There is ample fear being displayed this year!