Reporting by John Suddeth, CFA

“Inspiration is a guest that does not willingly visit the lazy.” -Peter Tchaikovsky

While floods of monies have rushed into IPOs this year, we are less sanguine on the immediacy of need for direct shipped organic baby food… None the less, Little Spoon was able to gather in $200 million of fresh capital. Also in the IPO maze, an electronic flying taxi (see photo), labeled as urban air mobility, garnered a $7 billion market cap. The time to final production for an electric air transport vehicle via the FAA process is daunting, never mind the serviceable market. If flying taxis seem like an anomaly, how about plopping capital into a glamorous hot dog-based restaurant chain? The IPO for Portillo’s Hot Dogs pushed the franchise to a $3.1 billion market cap. Not to be outdone by a vegetable focused restaurant, Sweetgreen, which jumped to a $4.3 billion market cap. Even Starbucks wasn’t immune, with a dynamic competitor, Dutch Brothers Coffee, coming in around $8.6 billion. We noted the lowest price to earnings ratio of the group at 316x earnings; all of a sudden Starbucks seems relatively cheap at 32x earnings.

If NGA doesn’t put monies in these IPOs, why the preoccupation? Well, it matters within the context of overall market dynamics, sentiments, volatility, and the skewing of relative comparisons. As such, we evaluate the deals bankers are presenting, staying attuned to directional flows and to the types of securities being consumed in the financial markets. The quality of the NGA diet, so to speak, hasn’t changed, but we can see from the caloric labels there’s a lot of “junk food” on the menu. What typically follows these overvalued IPOs is a period of indigestion, in the form of pivoting capital once the IPO excitement wears off, trade restrictions are lifted, stock options are exercised, and last but not least the financial reporting gets real. Analyzing deal flows lessens the risk of our making a knee jerk reaction during corrective periods and provides us the confidence to take on glaring opportunities in a mispriced world wholly distracted by any number of “busy” new offerings.

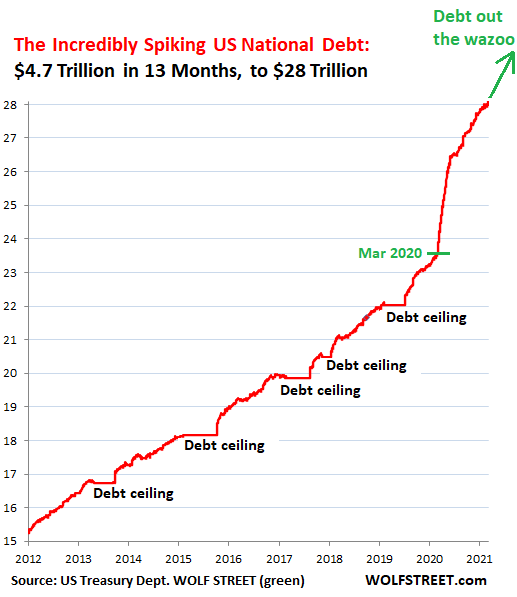

At $25 trillion plus, recognize there is no capacity, effective timeline, or political intention of ever “paying off” the U.S. debt. As an American taxpayer and business owner, it is perplexing to think in those terms (keep borrowing and never paying back) but as a global analyst, the reality of the situation is evident. That is, the U.S. government has the capacity to service, but not reduce with any measurable difference, the massive debt it has taken on the balance sheet. This circumstance remains a focal point of concern because of the associated interest rate impact in addition to the direction of the U.S. dollar and our purchasing power parity, as measured globally. When and exactly how this phenomenon is manifested is uncertain and feels problematic.

Finally, with a decade under our belt as an independent advisor, we have been experiencing generational transitions within our client base. While emotionally challenging to all, individuals and families are finding solace when they have a sound plan in place and an experienced team with known connections to the family. The passing of a matriarch or patriarch is heart wrenching but getting lost in corporate bureaucracy or a static legal system adds unnecessary delays and stresses. In our experience, generational transitions can occur smoothly with proper up-front planning and advisor familiarity with intent. If you seek additional guidance in this area (including a generational pow wow), please let us know. We are prepared to help.